Should I Establish A SEP IRA Or A SIMPLE IRA Plan For My Small Business?

Should I Establish A SEP IRA Or A SIMPLE IRA Plan For My Small Business? This flowchart will walk you through discovering your eligibility.

When it comes to selecting a retirement plan for your small business, the decision between a SEP IRA and a SIMPLE IRA can be critical. Let’s delve into the considerations to help you make an informed choice.

Understanding SEP IRA and SIMPLE IRA Plans

A Simplified Employee Pension (SEP) IRA and a Savings Incentive Match Plan for Employees (SIMPLE) IRA are both retirement plans tailored for small businesses. Each has its own set of features and eligibility criteria.

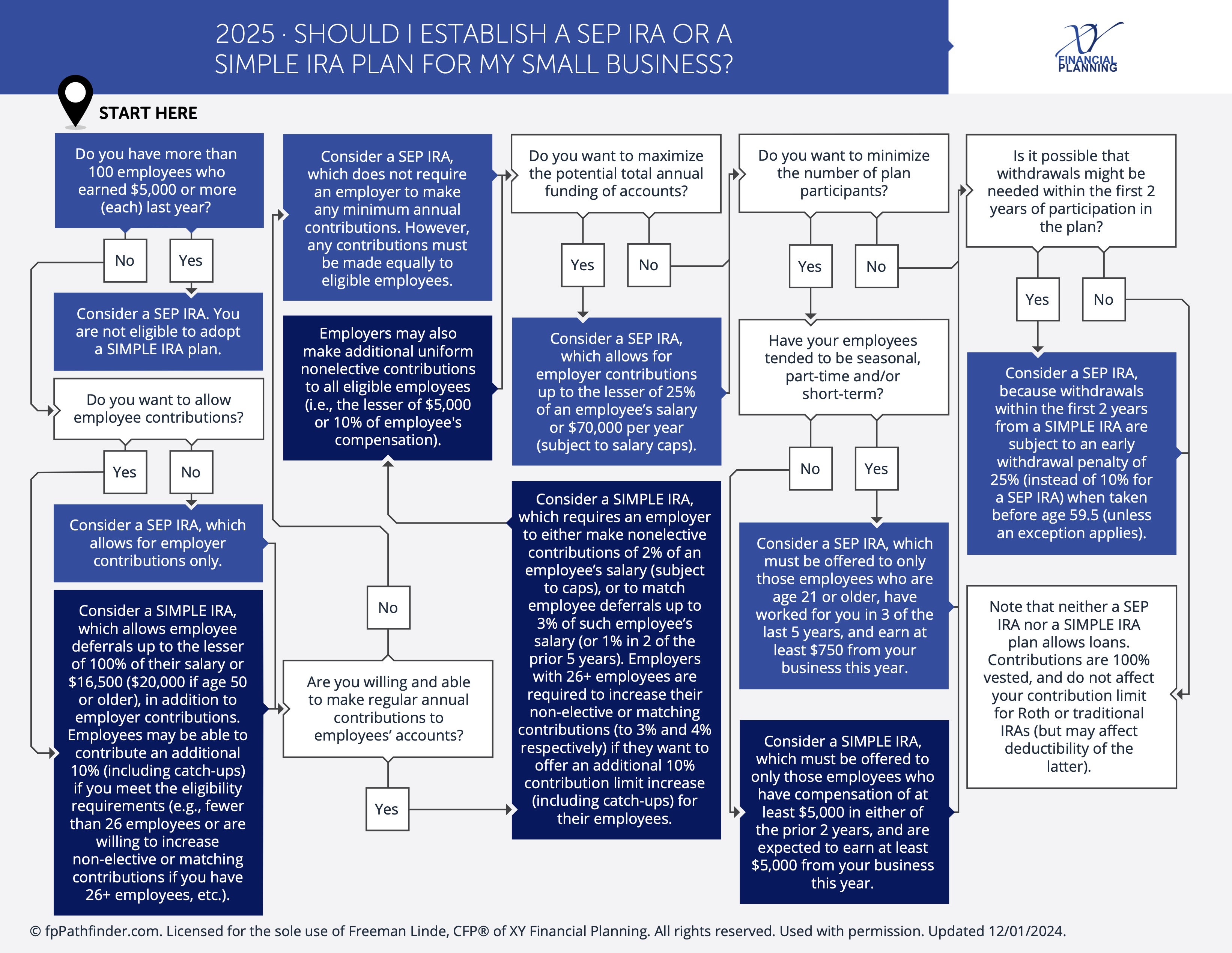

SEP IRA:

A SEP IRA offers a straightforward and flexible retirement savings option for self-employed individuals and small business owners. Contributions are made solely by the employer, with employees having no ability to contribute. Employers can contribute up to 25% of each employee’s compensation, up to a maximum of $61,000 in 2022.

SIMPLE IRA:

On the other hand, a SIMPLE IRA is designed to be more accessible for small businesses with fewer than 100 employees. Both employers and employees can contribute to a SIMPLE IRA. Employers are required to make either a matching contribution of up to 3% of each employee’s compensation or a non-elective contribution of 2% for all eligible employees.

Considerations for Choosing Between SEP IRA and SIMPLE IRA

- Employee Participation:

- If you want to provide your employees with the opportunity to save for retirement through payroll deductions, a SIMPLE IRA may be more suitable.

- However, if you prefer to have sole control over contributions and want to offer a retirement benefit without requiring employee contributions, a SEP IRA might be preferable.

- Contribution Limits:

- The contribution limits for SEP IRAs are generally higher, making them advantageous for businesses with higher profits.

- SIMPLE IRAs have lower contribution limits, which may be more manageable for businesses with tighter budgets.

- Administrative Complexity:

- SEP IRAs are relatively easy to set up and maintain, with minimal administrative requirements.

- SIMPLE IRAs have additional administrative responsibilities, such as annual employer contributions and providing employees with required notices.

Conclusion

Choosing between a SEP IRA and a SIMPLE IRA depends on your business’s specific needs and circumstances. Consider factors such as employee participation, contribution limits, and administrative complexity before making a decision. Consulting with a financial advisor can also provide valuable insights tailored to your business’s unique situation.

Should I Establish A SEP IRA Or A SIMPLE IRA Plan For My Small Business?

See more flowcharts here!

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.