Can I Do A Qualified Charitable Distribution From My IRA?

Can I Do A Qualified Charitable Distribution From My IRA? This flowchart will guide you through the eligibility factors.

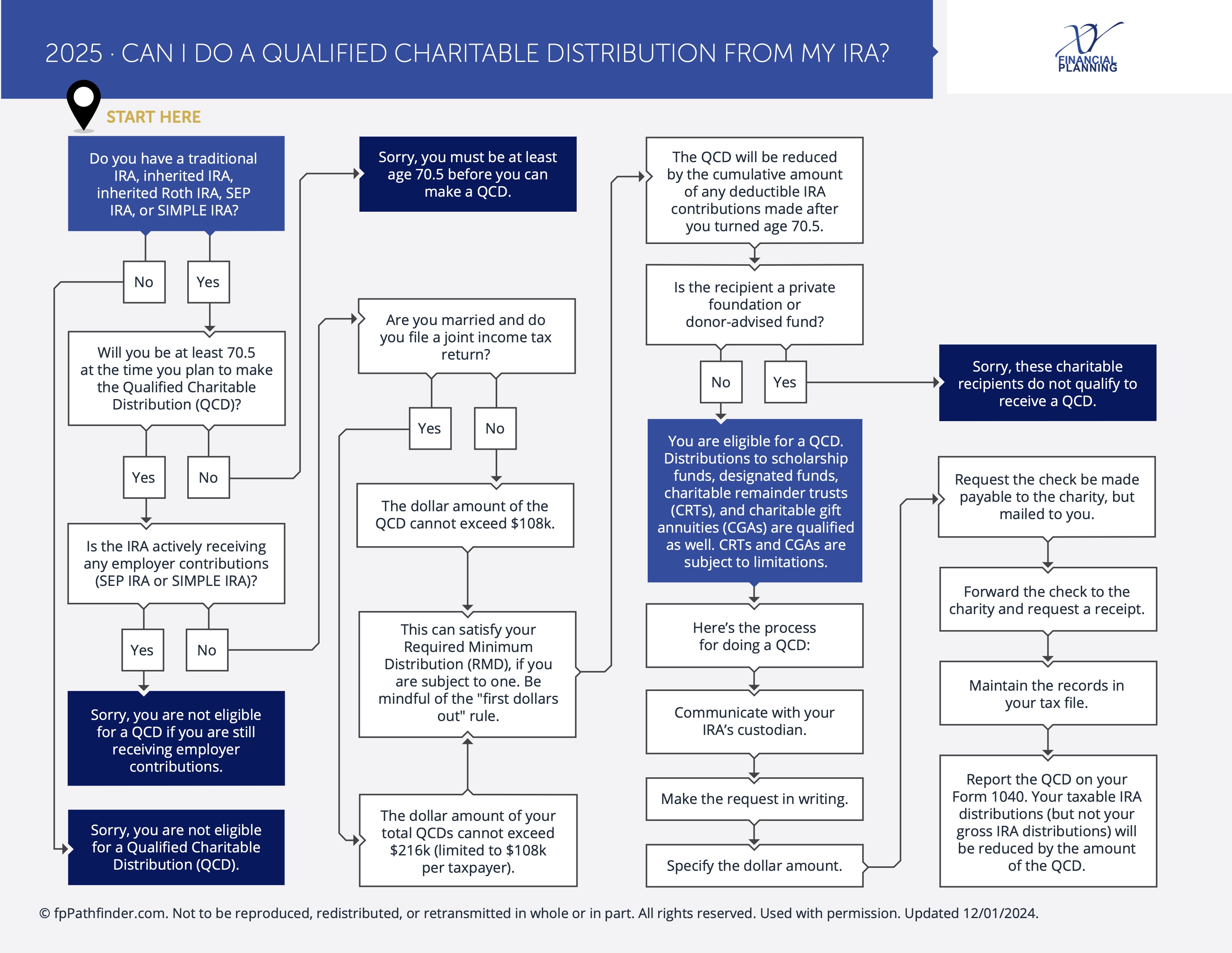

In the realm of charitable giving and retirement planning, grasping the nuances of Qualified Charitable Distributions (QCDs) from Individual Retirement Accounts (IRAs) is crucial. Whether you’re eager to support charitable endeavors while navigating tax implications, understanding the specifics of QCDs is paramount. In this piece, we’ll explore what QCDs entail, how they operate, and why they’re an appealing option for charitable contributions.

What is a QCD? A Qualified Charitable Distribution (QCD) refers to the direct transfer of funds from your IRA to a qualified charitable organization. This transfer satisfies your Required Minimum Distribution (RMD) obligation for the year without increasing your taxable income. This tax advantage makes QCDs particularly attractive for individuals inclined toward philanthropy and subject to RMDs from their IRAs.

How Does It Work?

Executing a QCD entails meeting specific criteria:

Age Requirement: You must be at least 70½ years old when initiating the distribution. Charitable Organization Eligibility: Funds must be transferred directly to a qualified charitable organization, excluding private foundations, donor-advised funds, and supporting organizations. Annual Limit: You can distribute a maximum of $100,000 per individual annually as a QCD. For married couples filing jointly, each spouse can contribute up to $100,000 from their respective IRAs. RMD Satisfaction: The distribution should fulfill your RMD obligation for the year.

Benefits of QCDs

Tax Efficiency: QCDs offer tax efficiency by not adding to your taxable income, potentially reducing your tax liability and adjusted gross income (AGI). Fulfillment of Charitable Intentions: QCDs enable you to support causes you’re passionate about while meeting RMD requirements, streamlining financial planning and enhancing the impact of your charitable contributions. Potential Estate Planning Benefits: By reducing your IRA’s value through QCDs, you may decrease your taxable estate, benefiting your heirs.

Considerations

Despite their advantages, consider the following factors:

Consultation with Financial Advisor: Given the complexities of tax laws and retirement planning, seek advice from a financial advisor or tax professional before proceeding with a QCD. Alternative Charitable Giving Strategies: QCDs are one option among several charitable giving strategies. Depending on your circumstances, alternatives such as donating appreciated securities or using donor-advised funds may be more suitable. Understanding IRA Withdrawal Rules: Familiarize yourself with IRA withdrawal rules, including penalties for non-compliance and potential impacts on eligibility for means-tested benefits.

Conclusion

Qualified Charitable Distributions (QCDs) from IRAs offer a potent avenue for supporting charitable causes while optimizing tax benefits. Leveraging the unique advantages of QCDs allows you to make a meaningful impact on your community while refining your retirement planning strategies. As with any financial decision, careful consideration and professional guidance are essential to ensure alignment with your overall financial objectives. Embrace the potential of QCDs to contribute meaningfully to causes close to your heart.

See more flowcharts here!

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.